TLDR

- Banks and bankers are not thrilled with the current state of stablecoins and regulation.

- They reportedly believe the tech is so good that it could trigger a bank run, potentially harming systemically important financial institutions.

- The current plan is to fight stablecoin legislation via lobbying efforts.

The banking industry is in panic mode. Banks are suddenly facing real competition from stablecoins. Their response so far? Lobbying for regulations to shut down the competition instead of improving their own services.

Traditional banking and the emerging stablecoin ecosystem are at odds with each other. On one side, you have banks trying to maintain their monopoly on deposits. On the other hand, you have stablecoins offering better yields and more transparent operations.

The crypto industry is no longer worried about regulation like it had to be during the previous administration. Things have never been better for it as a whole. And for some people, that has become a problem. Let’s get after it.

The Case For Banks

Banks aren’t going down without a fight. Their main arguments center around stability, regulation, and economic importance.

- Regulatory Protection – Banks operate under strict oversight from federal regulators. They’re required to maintain capital reserves, undergo regular examinations, and follow complex compliance procedures. That regulatory framework makes them safer than stablecoin issuers.

- Economic Role – Traditional banks serve as the backbone of credit creation in the economy. They take deposits and lend them out to businesses and consumers. This credit intermediation function makes them essential to economic growth.

- FDIC Insurance – Bank deposits are protected by federal insurance up to $250,000 per account. This government backstop provides peace of mind that most stablecoins can’t match.

The Case For Stablecoins

Stablecoins offer many things banks can’t. Or as some folks are arguing (more on that below), won’t.

- Better Returns – While banks pay close to 0% on most checking accounts and average .39% on savings, stablecoin platforms often offer 4-8% yields.

- Transparency – Stablecoins operate on blockchains, where every transaction is transparent and visible. You can verify exactly what backs your tokens.

- Innovation – The stablecoin ecosystem moves fast. New features, better user experiences, and higher yields appear regularly. Banks are still charging fees for basic services that should be free.

- Global Access – Stablecoins work 24/7, across borders, without the friction of traditional banking. No wire transfer fees, no waiting periods, no “sorry, we’re closed” messages.

How Banks Make Money

Banks have been running the same playbook for decades: customers deposit money, banks lend that money out at higher rates, and pocket the difference.

The average bank pays nothing on checking accounts while charging high interest (12% on average, even higher if you have bad credit, sometimes as high as 36%) on loans and credit cards. That spread is pure profit extracted from customers who have had no better alternatives.

But they do now…

Banks also generate massive fee income from overdrafts, wire transfers, ATM usage, and account maintenance. These fees disproportionately hurt lower-income customers who can least afford them.

The whole system depends on customers not having better options. Stablecoins change that equation completely. Smart contracts are not concerned with your credit score. A decentralized exchange doesn’t care about your income.

4 Reasons Why Banks Won’t Raise Rates

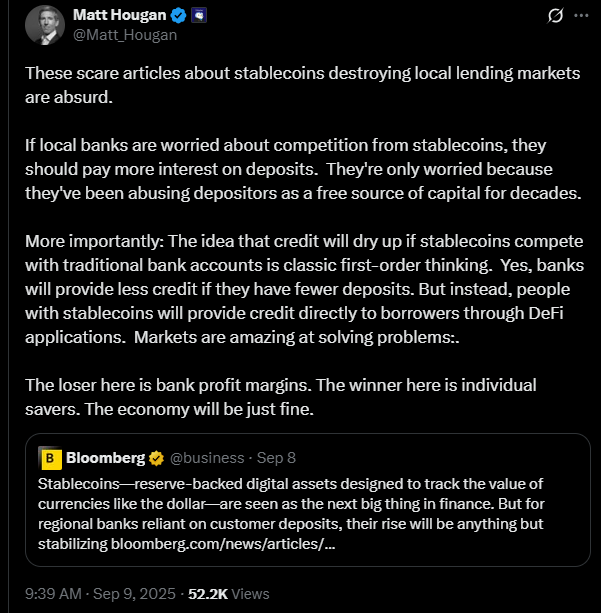

Matt Hougan, CIO of Bitwise, recently called out the banking industry’s hypocrisy. Banks claim they can’t compete with stablecoins, but they absolutely could raise deposit rates if they wanted to.

They don’t because:

1. Profit Margins Would Suffer

Raising rates would cut into the massive spreads they’ve enjoyed for years. Shareholders wouldn’t be happy.

2. Competitive Disadvantage

If one bank raises rates significantly, others would have to follow or lose deposits. It’s a classic prisoner’s dilemma where everyone benefits from keeping rates low.

3. Legacy Infrastructure Costs

Banks carry enormous overhead from physical branches, legacy IT systems, and compliance departments. They can’t operate as efficiently as blockchain-based stablecoin platforms.

Writer’s Opinion – Maybe they could start turning their lights off? Why does your bank need to be lit up like a Christmas tree at 3 AM on a Tuesday?

4. Risk Management

Higher deposit rates mean banks need to either accept lower profits or take more lending risk to maintain margins.

The Real Stakes

Banks have had a government-protected monopoly for so long that actual competition feels existential to them.

The banking industry’s own reports think that stablecoins could result in $6.6 trillion in deposit outflows. That’s not a sign of market instability — that’s customers voting with their wallets for better service.

Note: The full report mentioned above is behind a pay wall. We could not verify authenticity.

DeFi protocols are already showing how credit markets can function without traditional banks. Peer-to-peer lending, automated market makers, and yield farming provide alternative ways to match borrowers with lenders.

Banks profit from being middlemen, but markets don’t need middlemen when technology can connect parties directly.

What This Means For Users

If you’re new to crypto, the banks vs. stablecoins issue presents a clear opportunity. While traditional finance is trying to maintain the status quo, stablecoins offer:

- Higher yields on your savings

- More control over your money

- Lower fees for transactions

- Access to innovative financial products

The key is choosing reputable stablecoin platforms with proper reserves and transparent operations. Not all stablecoins are created equal, but the best ones significantly outperform traditional bank accounts.

The Future Belongs to Innovation

If banks want to hold on to their market share, they have to innovate and get back to putting a focus on their customers. They can no longer extract maximum value while providing minimal service.

Stablecoins represent the market’s response to decades of banking complacency.

The most likely outcome isn’t the death of banking, but a fundamental restructuring where banks must actually compete for deposits by offering real value. That’s good for everyone — for customers and capitalism as a whole.

The question isn’t whether the benefits of stablecoins will continue — it’s whether traditional banks can adapt quickly enough to remain relevant. And things aren’t looking good…

The revolution is happening whether banks like it or not.

About the Author