TLDR

- The UAE plans to release a CBDC by Q4 of this year.

- The country has been working on the idea for nearly two years. They believe blockchain tech provides more safety for users and will help prevent financial crime.

- The speed of blockchain transactions could promote more international trade with the country and attract more businesses.

The United Arab Emirates is gearing up for a major leap in its financial system with the highly anticipated launch of its digital dirham, a central bank digital currency (CBDC), slated for the fourth quarter of 2025.

The news has sparked interest among fintech enthusiasts, crypto investors, and newcomers eager to understand the growing role of blockchain technology in global finance. Let’s get after it.

What’s the Digital Dirham?

Not many folks in the US are familiar with the dirham. It’s the official currency of UAE, which you probably have heard about. From gold-plated Lambos cruising through the desert to it becoming the tech hub of The Middle East to becoming one of the biggest crypto hubs in the world — it’s on the level, as the kids say these days.

Writer’s note: We have no idea what the kids actually say these days. We just wanted to sound cool.

The digital dirham will be the first widely used CBDC. It is designed for easier, faster, and more secure transactions. According to The Khaleej Times, it will work hand-in-hand with physical cash and be accepted across all payment channels, effectively bridging the traditional and digital economies.

Central Bank of the UAE (CBUAE) Governor Khaled Mohamed Balama believes this rollout will go beyond just providing a digital payment method. He claims (while speaking to The Khaleej Times) that the digital dirham could improve financial stability and combat financial crime while opening doors for innovative products and services. It’s an ambitious pitch, no doubt.

Dypto Crypto’s Two Pennies

We try not to be haters. We try to keep an open mind and see how things play out before forming an official opinion. However, we’ve previously reported on the dangers that CBDCs could potentially present to users.

The government can track every move. They can freeze funds and accounts as they see fit. And that’s just the beginning. It’s a fully centralized digital currency.

It is not crypto. It uses blockchain.

We will always take the time to remind users that crypto and blockchain are not two sides of the same coin (buh dun tss). They are two completely different things.

That being said, maybe the UAE does it right. Given how forward-thinking they’ve been when it comes to other matters of fintech and tech in general, they could be on to something. When there were talks of making USD and Euro CBDCs, we cringed. But it’s possible that we were too focused on the worst-case scenario.

So while we won’t be using the CBDC for transactions for the above reasons, we will be watching it closely to see how well the nation pulls it off.

The History

The path to the digital dirham has been paved by impressive regulatory groundwork. In June 2024, the CBUAE approved a licensing framework for stablecoins, setting clear rules for issuance, supervision, and licensing of payment tokens. This move helped lay the foundation for blockchain-backed financial services in the country.

Tether, a major stablecoin issuer, was quick to capitalize on the framework. It teamed up with Phoenix Group and Green Acorn Investments to develop a dirham-backed stablecoin to provide a fully-backed digital representation of the country’s currency.

Why? Diversification. These days, Tether operates more like a country than it does a company.

And like most countries, it has a diverse portfolio of global currencies in its possession. It uses this treasury to back its stablecoins. Also, most of these funds are in government debt, so it makes quite a profit off of them as well.

Meanwhile, stablecoin adoption in the UAE is climbing rapidly.

Case in point? Circle’s USDC and EURC stablecoins became the first to be recognized under the Dubai Financial Services Authority’s crypto token regime earlier this year.

This didn’t just strengthen the appetite for stablecoins but also signaled the UAE’s readiness to play a major role in the global digital currency landscape.

*Sigh*

We need to back up for this next section and give a brief history lesson to set the tone a bit.

Back in 2022, TerraUSD promised a 20%-plus yield through its Anchor Protocol until its entire system crashed catastrophically. The fallout erased tens of billions of dollars’ worth of value, sending shockwaves through crypto markets. Many people lost life savings, which prompted regulators worldwide to act, mostly by overreacting.

Learning from such high-profile failures, the UAE’s cautious, regulated approach to launching the digital dirham and licensing stablecoins reflects a serious intention to avoid systemic risks.

By rejecting unstable algorithmic designs and instead focusing on fully-backed digital currencies, the UAE is aiming for safety and longevity.

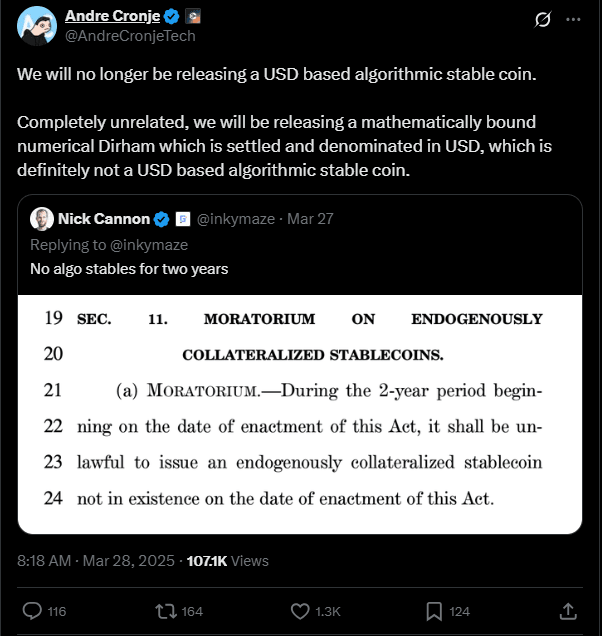

In (unfortunate) related news, it looks like algo-stables will be making a comeback with this CBDC.

Sonic Labs, which initially planned to launch a US dollar-pegged stablecoin, has quickly pivoted to dirham-denominated alternatives.

We could easily be wrong about CBDCs, especially given how much time and resources the UAE has put into doing it right.

But algo-stables? They simply do not work. Their design is inherently flawed.

But every time a new product is launched, there will be someone there looking to cash in somehow, some way. It looks like Sonic will be doing just that.

Why UAE’s CBDC Matters

Governments are no longer just observing the rise of digital currencies from the sidelines. They are stepping in and designing alternatives fully backed and regulated by their central banks.

For businesses, especially those in fintech and e-commerce, the digital dirham could mean fewer transaction costs, faster payments, and smoother cross-border trade.Sending money to another country could become as quick and cheap as sending an email. That’s the promise the UAE is tapping into, which will undoubtedly draw more international trade and become an even more welcoming place for companies (especially tech startups).

Additionally, the retail sector may find it a pleasant surprise, with its promise to simplify how customers pay by bridging digital wallets and traditional retail. The integration could fuel innovation, with businesses finding new ways to make payments seamless and efficient.

Recent moves like stablecoin regulation and supporting cross-border trade show that this isn’t just a lofty blueprint. The UAE appears to be laying the groundwork for making the digital dirham functional, practical, and adaptable to varied real-world scenarios.

For fintech enthusiasts and crypto-savvy individuals, the digital dirham embodies a shift toward greater acceptance of blockchain and digital currencies. Adopting a measured, carefully planned approach sets a standard for nations to integrate these technologies while addressing risks and building trust.

Provided they do it well. If they don’t, it could turn into an international catastrophe that politicians could use to fuel anti-blockchain sentiment.

Or maybe we’re overthinking it. Only time will tell.

We hope it works out. We really do. And we’ll be watching.

About the Author

Leaderboard

Only Top 10 users qualify for monthly $100 drawing.

| Rank | Points | |

|---|---|---|

1 1 | Jillianne R. |  119 119 |

| 2 | Phillip W. | 119 |

| 3 | Baffa O. | 119 |

| 4 | James C. | 119 |

| 5 | Male T. | 119 |

| 6 | Ron B. | 119 |

| 7 | Moses O. | 119 |

| 8 | Saifu A. | 119 |

| 9 | Lidya I. | 119 |

| 10 | Kofi K. | 119 |

| 11 | Mustafe O. | 119 |

| 12 | Musa S. | 118 |

| 13 | Dany T. | 118 |

| 14 | Lalisa F. | 118 |

| 15 | Ernest L. | 118 |

| 16 | Eric A. | 118 |

| 17 | John P. | 118 |

| 18 | David D. | 118 |

| 19 | Barry S. | 118 |

| 20 | Genuine C. | 118 |

| 21 | Dan B. | 118 |

| 22 | James A. | 118 |

| 23 | Menelik G. | 117 |

| 24 | Kyakonye S. | 117 |

| 25 | Asfaw I. | 117 |

| 26 | Khaleeq A. | 117 |

| 27 | Wayne C. | 117 |

| 28 | Mohamed N. | 117 |

| 29 | Hamza K. | 117 |

| 30 | ALIYU Y. | 117 |

| 31 | Soly N. | 117 |

| 32 | David B. | 116 |

| 33 | Nathan H. | 116 |

| 34 | Nour E. | 116 |

| 35 | Bello U. | 116 |

| 36 | Nazeeh K. | 116 |

| 37 | Anselme D. | 116 |

| 38 | Muhammmad H. | 116 |

| 39 | Sherry D. | 116 |

| 40 | Abubeker A. | 116 |

| 41 | Kenneth J. | 115 |

| 42 | Carlos M. | 106 |

| 43 | William M. | 105 |

| 44 | Okello A. | 105 |

| 45 | Obey T. | 101 |

| 46 | Michael R. | 101 |

| 47 | Lucy A. | 99 |

| 48 | David C. | 98 |

| 49 | Hilik T. | 98 |

| 50 | Gabrielle G. | 97 |

| 51 | Kimberley S. | 95 |

| 52 | Mich O. | 94 |

| 53 | Oyetunji S. | 93 |

| 54 | Latrice S. | 92 |

| 55 | THEOBALD S. | 92 |

| 56 | hanad A. | 84 |

| 57 | Pavan C. | 84 |

| 58 | Kyarugaba S. | 83 |

| 59 | Michael M. | 82 |

| 60 | Rosalio S. | 82 |

| 61 | Tha H. | 82 |

| 62 | Hossana E. | 82 |

| 63 | John H. | 82 |

| 64 | PaulShultis S. | 64 |

| 65 | Gashaw N. | 63 |

| 66 | Jeremiah A. | 63 |

| 67 | Alam Z. | 62 |

| 68 | FRANK I. | 61 |

| 69 | Melkamu A. | 61 |

| 70 | Akeem A. | 58 |

| 71 | OSAMEDE O. | 56 |

| 72 | Isaac O. | 56 |

| 73 | Olorunwa M. | 56 |

| 74 | Yashin S. | 55 |

| 75 | Erbs M. | 55 |

| 76 | John S. | 55 |

| 77 | Shiferaw T. | 54 |

| 78 | Richard P. | 54 |

| 79 | Mbongiseni S. | 54 |

| 80 | Christian C. | 54 |

| 81 | james_bolinda | 54 |

| 82 | Ronald H. | 53 |

| 83 | Sean S. | 43 |

| 84 | Kenneth B. | 42 |

| 85 | Aimee B. | 40 |

| 86 | Jamil B. | 40 |

| 87 | Muhammad I. | 37 |

| 88 | Expert E. | 36 |

| 89 | Raz E. | 36 |

| 90 | Juma G. | 35 |

| 91 | Shom S. | 35 |

| 92 | Somadina O. | 35 |

| 93 | Carlos P. | 35 |

| 94 | Kenneth J. | 35 |

| 95 | Ade N. | 35 |

| 96 | jtcraw | 35 |

| 97 | Bekele W. | 32 |

| 98 | Glen M. | 32 |

| 99 | DAVISON P. | 31 |

| 100 | Martins M. | 31 |

| 0 |

Countdown to next draw

days

hours

minutes

seconds