What is a Public Blockchain?

A public blockchain is a decentralized protocol that anyone can join and participate in.

The Long Definition

A public blockchain is a distributed ledger that is openly accessible to everyone. Anyone can join and participate in the activities of the protocol. They can complete transactions, help validate transactions, audit the network, etc. This is regardless of their job, status, location, age, etc.

Today, most popular blockchains are both public and permissionless. Examples include Bitcoin, Ethereum, Cardano, Avalanche, Polkadot, Binance Smart Chain (BSC), etc. A common feature among them is their ability to process and record cryptocurrency transactions.

History of Public Blockchains

In 2008, an anonymous person or group called Satoshi Nakamoto released a whitepaper. The paper was titled “Bitcoin: A Peer-to-Peer Electronic Cash System.” It described a trustless, decentralized system for conducting transactions over the Internet. The system was designed to allow anyone, anywhere in the world to send and receive money.

This was the Bitcoin blockchain– the first public blockchain in history. Since its launch, many other blockchains have been created and released. The most popular of these are Ethereum and BSC. Like Bitcoin, they are open to anyone who needs to use them.

Understanding Public Blockchains

Public blockchains are defined by the following characteristics:

- Distributed architecture: A public blockchain runs on a network of nodes (computers) rather than a single server. The nodes are typically spread out in different locations across the world.

- Decentralized: Public blockchains are not owned by anyone, not even the creators. There is no centralized control/ownership. Instead, such a network is collectively managed by its community. All proposals must pass through the community before they are actualized. This happens through nodes.

- Open source: It usually takes one or two teams to build a public blockchain. But once the protocol goes live, it becomes open source. This means that any developer with the necessary skills can contribute to its development. They can help discover and fix bugs and implement new features to the protocol.

- Permissionless: Public blockchains are decentralized. Therefore, you don’t need anyone’s approval to use one. You can participate in the network as long as you have an internet connection. This is what is meant by permissionless. It is what makes these protocols ‘public’.

- Transparent: Public blockchains typically operate on a policy of complete transparency. This means that the data they store is visible to everyone. For example, you can use blockchain explorers to see the full history of transactions on the Bitcoin blockchain.

How Do Public Blockchains Work?

A blockchain is a distributed ledger. In the case of most public blockchains, it is a distributed ledger of transactions. For example, Bitcoin keeps a record of BTC transactions while Ethereum records ETH.

As stated above, these protocols are decentralized. No one person or entity owns/controls the network and anyone can participate. So, how do they make sure that things run smoothly while remaining public and decentralized? How do they ensure that they only record valid transactions and make the right improvements?

In short, public blockchains use several mechanisms to keep themselves in order. These include consensus mechanisms, reward programs, and democracy.

Consensus Mechanism

A consensus mechanism is a technique used by protocols to verify data before it is added to the blockchain. There are many different types of consensus mechanisms. However, the premise is largely similar– for data to be considered valid, the majority of participants must agree that it is. They must reach some form of consensus.

How this consensus is arrived at varies from blockchain to blockchain. The two most popular techniques are Proof of Stake (PoS) and Proof of Work (PoW). The former uses validators to confirm transactions while the latter uses miners.

Anyone can become a validator/miner. However, there is a certain cost associated with this level of participation. This cost is there to encourage good behavior. For example, validators are required to lock a certain amount of cryptocurrencies in the protocol. Miners, on the other hand, must invest in expensive equipment that uses lots of power.

Rewards

Most people voluntarily participate in public blockchains. Naturally, volunteers don’t expect to receive payments. But some functions are so crucial, take a lot of time, and can cost a lot of money. For example, verifying transactions requires the participant to buy expensive equipment or lock up a significant amount of crypto in the protocol.

So, how do public blockchains incentivize people to do these jobs?

Through rewards. Participants are rewarded for being part of such crucial functions. In the above example, miners receive newly minted cryptocurrency for every block they verify. These are known as block rewards. Similarly, validators receive a portion of the transaction fees for the transactions they help confirm.

Another example of public blockchains using rewards is in finding bugs and security vulnerabilities. Bug hunting takes a lot of skill and time. To encourage more developers to participate, some blockchains run bounty programs. These are programs that reward developers with crypto for every bug and vulnerability they discover on the protocols.

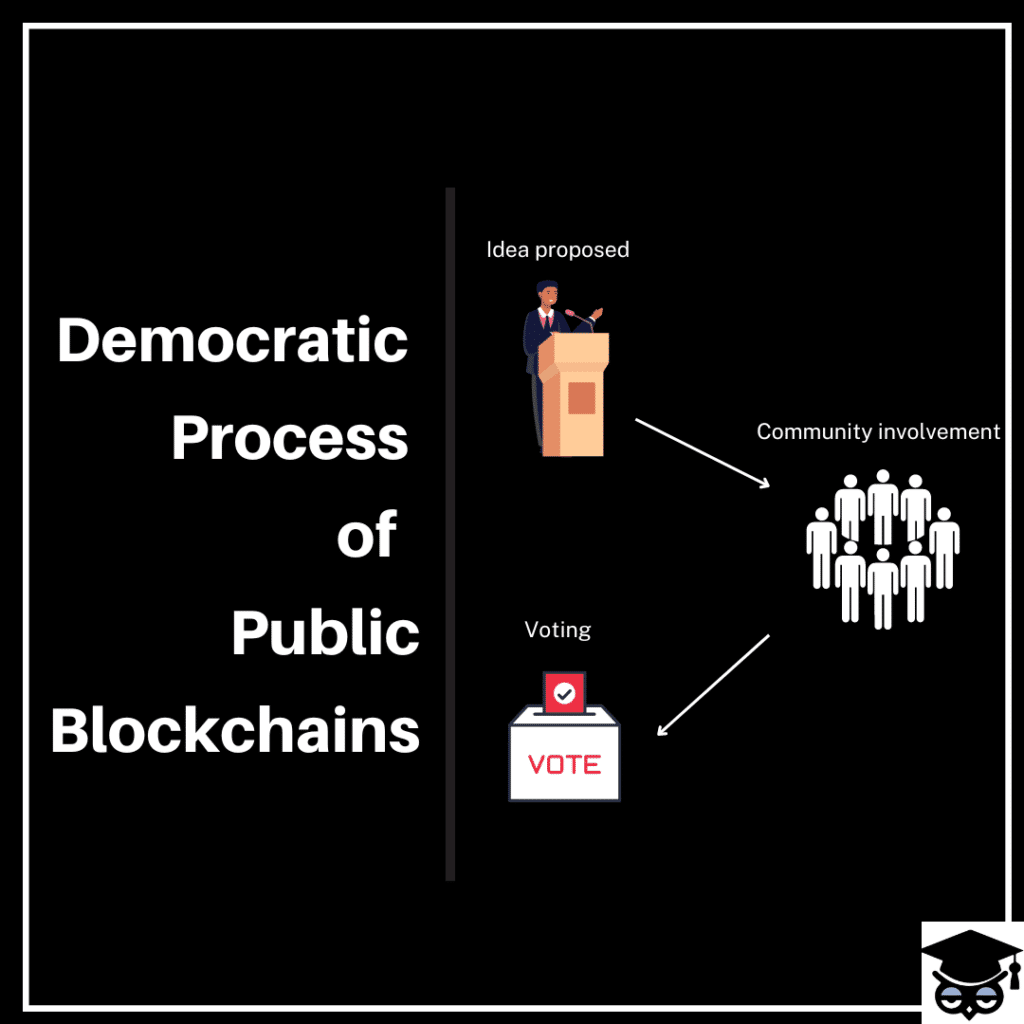

Democratic Process

Public blockchains operate like democracies. Rather than having one person/body make all decisions, the community is involved. Through voting, members decide on the overall direction of the protocol.

The decision-making process resembles something like this:

- Someone proposes an idea, a change or a new feature to be added to the blockchain. Some blockchains have procedures for submitting proposals. For example, Bitcoin has Bitcoin Improvement Proposal (BIP). Ethereum has Ethereum Request for Comment (ERC).

- The proposal goes through the community. Members are given some time to examine and question it.

- They then vote on it. If the proposal passes the vote, it will be implemented. If not, it will not be implemented.

What are Public Blockchains Used For?

Today, public blockchains are primarily used in crypto. They provide the underlying technology that allows digital currencies to exist and function. This is why a blockchain is often referred to as a ledger of cryptocurrency transactions.

Some public blockchains have taken this a step further by being programmable. This has allowed for the development of decentralized applications (dApps). For example, Ethereum has the Ethereum Virtual Machine (EVM). EVM provides a platform for running smart contracts and dApps.

About the Author