What is an NFT?

A non-fungible token (NFT) is a unique digital item on a blockchain. Non-fungible means that they are not interchangeable. Each item is unique, has its own value, and therefore, cannot be equally exchanged for another item.

NFTs have a growing number of applications. These include digital artwork, blockchain-based gaming, virtual worlds, and club memberships. As blockchain adoption grows, NFTs have begun to incorporate some real-world applications as well. Some of the industries expected to embrace them include real estate and event ticketing.

History of NFTs

Blockchain technology went mainstream in 2009 with the launch of the Bitcoin blockchain. However, NFTs weren’t really a thing until after the creation of Ethereum. This is because Bitcoin doesn’t support the building and creation of other assets on its network.

On the other hand, Ethereum has smart contracts(link to smart contracts). These allow developers to build and deploy their own tokens on the blockchain.

CryptoKitties by Dapper Labs is the first popular implementation of NFTs. The project was launched in 2017 on Ethereum. It is a blockchain-based game that consists of unique digital representations of cats. People use Ether (ETH) to buy, raise, breed, and trade these kitties.

Since then, thousands of NFT projects have been launched. The most popular of these include Cryptopunks (also launched in 2017), Decentraland, and Bored Ape Yacht Club (BAYC).

In 2021, NFTs became some of the hottest items in the digital asset space. The value of individual pieces skyrocketed thanks, in part, to the crypto bull market.

Notable pieces from this period include Beeple’s Everydays and Pak’s The Merge. These sold for $69.3 million and $91.8 million respectively. There is also an NFT of Jack Dorsey’s first tweet. It sold for more than $2.9 million.

Fungible vs non-fungible

NFTs’ defining feature is that they are non-fungible. This means that each NFT is totally unique. It has a unique identifier that distinguishes it from other tokens. Therefore, two NFTs are not interchangeable. You cannot exchange one NFT for another and still have the same value, as you would a dollar bill.

A dollar bill, in this example, is fungible. This is because the value of one dollar bill will always be equal to that of another. So the two are interchangeable. You can directly swap one with another without losing value.

How do NFTs work?

NFTs are digital assets stored on a blockchain. They are created through a process called minting. Minting involves writing a digital item to a blockchain.

It can be done on a marketplace, like OpenSea, with only a few clicks. Here, the marketplace does the programming for you. Your job is just to upload the picture or piece of digital art you want to turn into an NFT.

There is, of course, a more complex way. You input all the necessary information and incorporate the smart contracts yourself. This is only possible if you’re familiar with blockchain programming languages like Solidity, though.

It’s important to note that there are standards for creating tokens on Ethereum. A standard is essentially an outline that developers follow when minting tokens. Having a common standard makes token creation easier and ensures that the assets can be used across different protocols on the chain.

For NFTs the commonly accepted standard is ERC-721. There is also ERC-1155, which improves on ERC-721 by allowing you to write a single smart contract for multiple tokens.

Like every other crypto token, NFTs can change ownership. Each NFT is associated with a particular blockchain address. This address belongs to the owner of the asset. When the owner sells and/or sends the NFT, they change the address that it’s linked to.

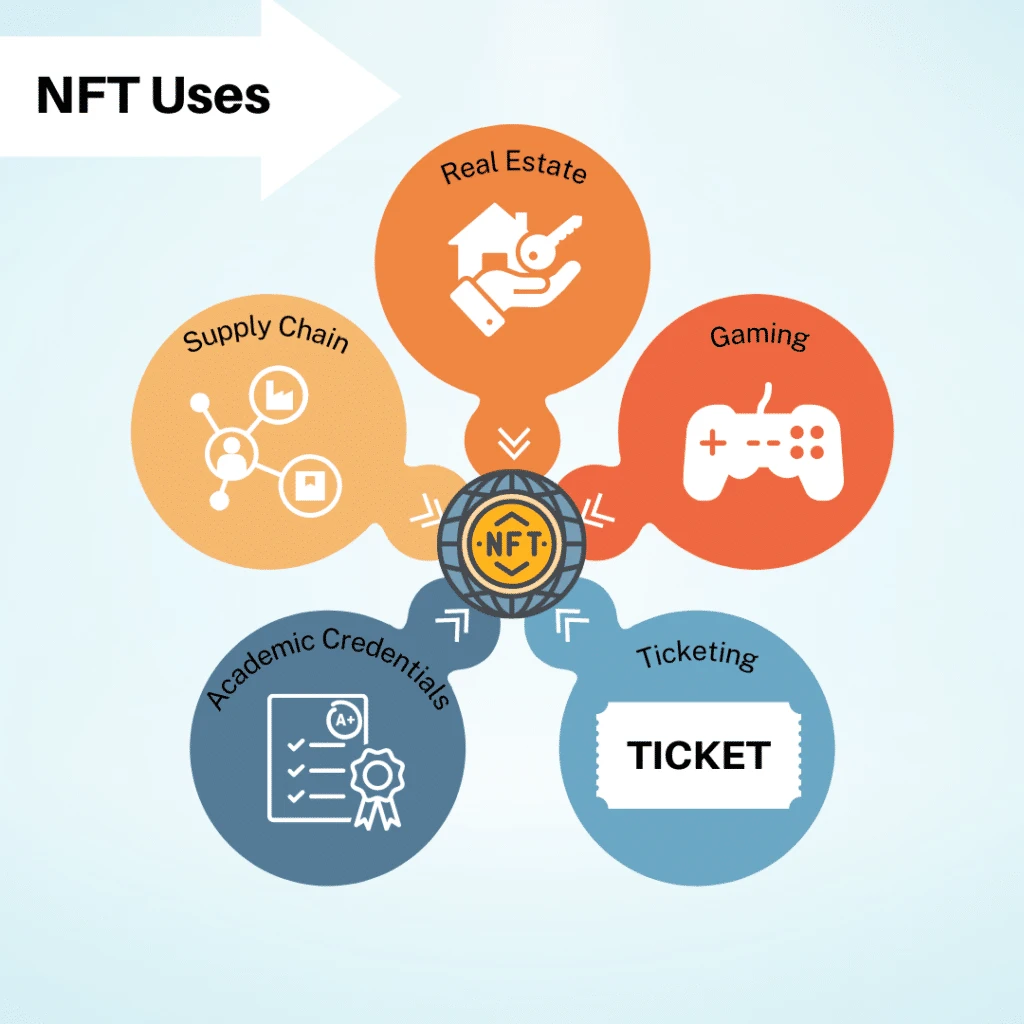

NFTs Uses

NFTs can be used to represent any unique items on the blockchain. And, anyone that owns the NFT owns the real item. For instance, each piece of art is unique. So currently, most NFTs represent a piece of digital art. Anyone that owns the NFT also owns the art it represents.

Using this same principle, NFTs have potential applications in several industries. These include intellectual property, identity management, and real estate. Experts predict that in the future, title deeds will be tokenized into NFTs. Tokenization is the process of turning an item into a token on the blockchain.

NFTs are also being used to show club membership. Take the BAYC for instance. Owners of BAYC NFTs belong to a club where members access exclusive benefits. Many similar clubs exist all around the world.

Another use of NFTs is in Web3 gaming and virtual worlds. This involves tokenizing in-game items. It allows real ownership of items that players earn and buy inside a game. And since blockchain games can be interoperable, players would be able to use items across multiple games.

About the Author