TLDR

- In a recent article featured in the NYT, two authors discuss why the American people should be concerned about President Trump and the crypto industry.

- The authors are John Reed Stard and Lee Reiners. Both have connections to Duke University and are advocates for the SEC’s “regulation by enforcement” stance of the previous regime.

- This article is full of inaccuracies and fearmongering. Luckily, we’re here to break it down, point by point.

Today’s article is in response to a recent opinion piece that appeared in the New York Times this weekend. It is co-authored by two gentlemen, John Reed Stark and Lee Reiners.

We’re going to break down this article and provide our two pennies. This one’s going to be a doozy. Let’s get after it.

The Opening Argument — The Crypto Industry Backing Trump’s Presidency

“Cryptocurrency moguls heavily backed Donald Trump’s bid for the presidency, and he has already begun to pay them back by deregulating the crypto industry….”

This is partially true. The crypto superpac Fairshake handed over $100 million to candidates in the recent election. However, it wasn’t to have the industry deregulated. Quite the opposite.

It was because the industry wanted regulation, which it had been denied for years via Operation Chokepoint 2.0.

All the industry wanted was to be treated fairly, which President Trump and many states are now actively working on.

It’s important to note that SBF illegally donated somewhere between $40 and $100 million to political campaigns, most of which went to democrats. It seems pretty convenient that both the authors as well as current politicians always seem to forget about that (It probably just slipped their minds, kind of like the cash that got slipped into their pockets).

“Combined with Mr. Trump and his family’s own dive into the market, that may enrich him and his circle. But it may also worsen all kinds of criminal activity and risk the health of our financial markets.”

First off, no one invests money to not build wealth, right? Did anyone reading this get into crypto to be poor? We didn’t….

Why are so many of the president’s enemies focused on his crypto holdings? The man is a billionaire, and only a fraction of that is involved with the crypto industry. He was a businessman before he became a politician. Did people think he would stop being a businessman?

And it’s not like other politicians don’t make money in financial markets. Hillary Clinton (quite famously) turned $1,000 into $100,000 in less than a year. This was in 1978, by the way.

Adjusted for inflation, that would be just a hair shy of half a million dollars. We’re 100% sure it was beginner’s luck. There’s no way that Mrs. Clinton would involve herself with anything nefarious. We refuse to believe such a thing.

She’s not the only one. While this article is a bit dated (it’s ten years old), it shows the changes in net worth of several politicians since they were elected. The person at the top of the list had their net worth increase over 70,000% in under a decade.

Nancy Pelosi has an estimated net worth of around $250 million and has been accused of insider trading activity. Multiple times.

Even if she isn’t, her incredible performance can be summed up with the term “highly controversial”.

In a perfect world, politicians shouldn’t care about making money. But this world isn’t perfect. Delaware must come close, though. That’s probably why both President Trump and Hillary Clinton have shell companies registered there.

So yes. Trump wants to make money in crypto just like everyone else. Thank you for the exit liquidity, Mr. President.

The Next Set of Blatant Half-Truths

“In the last several years, the Securities and Exchange Commission was moving to regulate crypto, recognizing its potential to destabilize traditional finance…”

True! They set out to destroy the industry by not providing or setting clear guidelines, and then prosecute businesses in the industry at their convenience.

Also…that’s not their job.

And also…true on their next point. It does have the potential to destabilize traditional finance.

(You’d think these authors are new. They aren’t. We’ll get to that in a bit.)

Mr. Trump has ended this tradition. In little more than three months, the S.E.C. has eliminated its crypto-enforcement program, dismissing, closing or “pausing” nearly every crypto-related lawsuit, appeal and investigation…”

True. We sent a thank-you letter and a fruit basket.

Next, the authors got a bit redundant. We’re going to skip the next paragraph entirely.

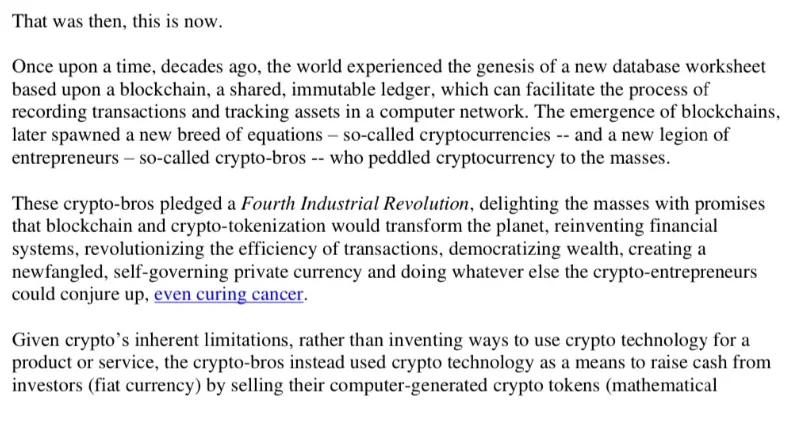

“For 16 years, crypto enthusiasts have promised a “fourth Industrial Revolution,” pledging that crypto technology would transform the planet by democratizing wealth. Yet while other digital payment systems backed by established financial institutions, like Apple Pay, have flourished, cryptocurrency has yet to prove that it has any practical and legitimate utility.”

*Sigh*

False. False. False. False. And…false.

These are a few articles that we’ve written over the last few months. If we posted a link to every current and potential use case for crypto, we’d be posting links in this section all day. And ain’t nobody got time for that.

Furthermore, the reason crypto hasn’t had the success of Apple Pay is that the SEC, DOJ, and FDIC were actively trying to shut the entire industry down. And if Trump hadn’t been elected, they very well could have succeeded.

Finally…Some Accurate Information…Kind Of

“Instead, what cryptocurrency has given our world is a shield that facilitates crime, from sex trafficking to ransomware attacks, drug dealing to child pornography. North Korea has become a crypto superpower, stealing over $6 billion worth of crypto through hacking over the past decade. By using unregulated offshore exchanges to convert the stolen crypto into cash, North Korea has funded its nuclear weapons program and shored up its sanctions-ravaged economy.”

This is true. We’ve covered the Lazarus Group quite a bit. And everyone in the industry admits they’re a problem. But these guys are some of the best hackers in the world. It’s an unfortunate truth, and we still have work to do security-wise.

No one is claiming blockchain or smart contracts are perfect solutions. We’re just claiming they’re better than the current ancient systems.

The Real Truth

No single currency is used for illicit activity more than the US dollar.

Oh snap. We just went there.

One report from Money and Banking estimated that as much as 3/4s of all $100 bills are located outside of the US and used for illicit activity. There are two reasons for this.

- Weight: a million bucks fits into a suitcase and only weighs about 20 lbs.

- Track proof: Unlike blockchain tech, cash can’t be tracked. If you hand $20 to a buddy who hands it to a buddy, that money is gone forever. You don’t know who it went to or what they’re doing with it. Neither does the US government.

Chainalysis, back in 2020, estimated that less than 1% of Bitcoin transactions were linked to bad people doing bad things.

The same can’t be said for USD, with illicit activity usage around the $2 trillion mark. Yes. Trillion.

A gentleman named Kenneth Rogoff wrote a book called “The Curse of Cash”. You probably haven’t heard of him. He’s a professor at Harvard, a chess champion, and a former Chief Economist at the International Monetary Fund.

So not a big deal or anything…

In his book, he estimates that around one-third of all cash is unaccounted for. As in…no one knows where it is or who has it. In his opinion, this money is being used for illicit activity and tax evasion.

Cartels count their money by weighing it. It’s driven across the border with 18-wheelers and put on a scale. It’s estimated that the cartels alone brought in a cool $13 billion in 2021, mostly from drugs and human trafficking.

Due to a lack of available information, we couldn’t find accurate figures for the amount of estimated crypto used for illicit activity in 2021 to make a comparison.

However, according to TRM Labs, overall crypto transaction volume was around $10.5 trillion in 2024, with an estimated $45 billion of that, or .4%, used by criminals. This was a 24% drop from 2023. The biggest reason is likely that criminals are figuring out exactly what “public ledger” means.

We aren’t saying criminals don’t use crypto. We aren’t saying criminals can’t launder money with it. We’re saying that criminals using crypto represents a tiny fraction of criminal activity in the world and a tiny amount of crypto transactions.

And these authors are clearly using it inaccurately as a selling point for their article.

Then the article has a bit more redundancy, talking about FTX…we’ll be skipping that section as we’ve already covered it.

More Blatant Inaccuracies…Because…Why Not?

“That was before the second Trump term. The S.E.C. suspended its civil fraud case against Binance in February. Company executives have met with Treasury Department officials to discuss loosening government oversight, The Wall Street Journal reported, while Binance has been exploring a deal to list a new cryptocurrency from a venture backed by Mr. Trump’s family.”

Wow. False. The authors are mentioning an article from a couple of months ago. We looked into it and actually wanted to report on it. But we could not find any evidence at all that supported the author’s claim.

It was entirely made up as part of a political smear campaign (as far as we could tell). Language used were phrases such as “according to a source close to the matter”.

Nope. That’s not journalism. That’s not news. If you can’t name names, provide sources, or give readers some sort of public receipt to research the information themselves, you aren’t doing your job as a journalist.

“Crypto is also making more inroads into the world of traditional finance. Last month, federal regulators reversed a policy that required banks to obtain approval before offering crypto-related products and services. And both the House and Senate are debating bills that would provide a new regulatory framework for stablecoins, a type of crypto intended to maintain a stable value and allow for easier trading of different crypto currencies, with the aim of further integrating them into the banking system.”

These are the first accurate statements these guys have made. However, we don’t think they noticed the contradiction between saying things like “crypto is also making inroads into the world of traditional finance” and “cryptocurrency has yet to prove that it has any practical and legitimate utility” (just a few paragraphs above).

Not sure if anyone else caught that. But it gave us a good chuckle.

Anywho. We reported on the topics these guys mentioned above. You can read up on what they’re talking about here and here. The TLDR? The US government is getting with the crypto program and working on legislation that will help with innovation and protect consumers, which is what they should have been doing in the first place.

“This state of affairs brings to mind a similar moment in our history — the 1920s, when insider trading, market manipulation and lack of transparency destroyed public confidence in the system and helped set off the stock market crash that in turn played a part in the Great Depression. The S.E.C. was created to restore trust and bring order to our capital markets, something it did for the next nine decades.

By directing the S.E.C. to abdicate its critical mission of investor protection, Mr. Trump is unnecessarily endangering our financial system. Whether he is doing so to keep his promise to crypto-donors or in a zeal to cash in (or perhaps even both), that is a troubling development not just for investors and banks, but for all of us.”

Oh really? So you guys were around back then? You remember how things were “back in the day”? C’mon.

The threats the authors are referring to are incredibly limited in today’s financial ecosystems, thanks to modern technology…such as computers, phones, and running water.

This comparison isn’t even close to fair. So what is it? Fearmongering. Plain and simple.

There is nothing wrong with the SEC or the DOJ. The issue is that these agencies were doing something that wasn’t their job.

The previous administration created a war on the crypto industry and used the SEC, the FDIC, and the DOJ to do it. All that has happened is that they are no longer doing that. That’s literally the only thing that has changed. Now, those agencies are back to doing the jobs they were designed to do in the first place.

About the Authors

How are Mr. Stark and Mr. Reiners connected? What’s their deal? What makes them enough of an expert to write this piece and have it published in the New York Times? Both of them are connected to Duke University. Reiners is a professor and Stark was one until 2024. That’s the most likely connection.

Lee Reiners

Reiners is still at Duke. He’s had a lot to say about crypto over the years, most of which was either founded in ignorance…or possibly outright lying.

Bitcoin is too volatile to ever be legal tender, says Duke’s Lee Reiners

This one is pretty funny. This video was made at the absolute peak of the last bear market, with BTC worth around $20k.

Around fifteen seconds into that clip, he says, “It’ll be worth no more than $1,500 in five years…It has to be useful for something. And we haven’t seen it yet…I don’t see it having any value.”

He goes on to make some solid points, though. He’s right that BTC will never be legal tender in the US. Luckily, it’s not supposed to be. It’s an asset class. Not a replacement for the dollar.

Many people are under the assumption that it’s a possibility. The chances are pretty slim that this could ever happen. It’s highly unlikely that the US government will allow anything aside from the dollar to be legal tender.

You will probably never go into Walmart and be allowed to spend BTC at the register. The same is true for the euro, the Singapore dollar, the Indian rupee, or any other currency.

That doesn’t make Bitcoin any less of a currency or an asset class.

Dazed and Confused: Breaking Down the SEC’s Politicized Approach to Digital Assets (EventID=117661)

You’d think after Bitcoin went through the roof, Blackrock got on board, ETFs went live, and many other positive changes, Mr. Reiners would change his tune a bit. He hasn’t.

In this clip from about seven months ago, his presentation begins during the 36th minute. His presentation begins by talking about narratives and mentions the Fairshake donations.

He says, “The story they (the crypto industry) tell is simple, powerful, and false…there are millions of one-issue pro-crypto voters who stand ready to support the candidate that embraces crypto…”

Correct. And they were right.

He later adds, when speaking about President Trump’s campaign, “He would make the US the crypto capital of the planet and fire SEC Chain Gary Gensler on day one.”

Partially true. Gensler stepped down. But yeah, so far, Trump is keeping his word. But then…Mr. Reiners goes off the rails a bit. He states, “The reality is that very few Americans use or own crypto.”

This is wrong. The actual reality is that over 20% of Americans own crypto.

He continued, “…There’s no evidence to suggest that their vote is principally influenced by candidate stance on cryptocurrency…”

Whelp. Trump won. So the industry must have done something right. Because so far, he’s been true to his word.

Towards the end of his testimony, we found another key link between Reiners and Stark, when he says, “…The SEC has resisted industry lobbying and upheld the securities laws established by Congress 90 years ago. In my written testimony, I offer context for ongoing debates about the SEC’s role in cryptocurrency markets by examining the agency’s longstanding, consistent, and legally sound methods of cryptocurrency enforcement and regulation.”

Technology, innovation, and modernization always impact laws. In the section above this one, the authors mention things happening in the 1920s. That’s right around the time women were allowed to vote. People of color were separated from the rest of society. Laws were enacted to prevent non-European, non-whites from immigrating to the country. Disabled people could be sterilized for being…yeah…disabled.

So yeah. Laws change as society changes. As tech changes.

Mr. Reiners is of the opinion that regulation by enforcement is the SEC’s job. It’s why they exist. And that isn’t true.

Lastly, he fails to mention that the SEC was operating under the assumption that all cryptocurrency falls under a security. But the reality is that we are dealing with something much more complex than the scope of the SEC and even the Commodities Regulators.

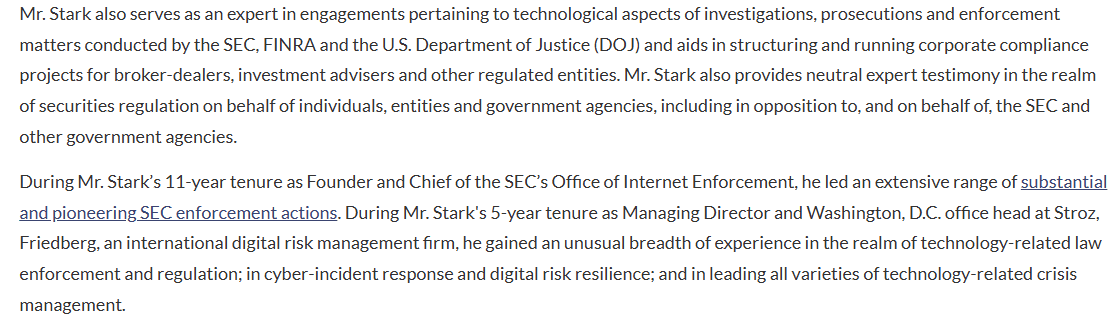

John Read Stark

Stark is the former Chief of the SEC’s Office of Internet Enforcement until 2009. He’s held law professor positions at Duke and Georgetown and is now a consultant.

There isn’t much information on him. Some of what we did find was a bit disturbing. Other tidbits of information led us to think that he may have, until recently, been working with the SEC as an independent contractor.

If this is the case, it could definitely explain why he’s so salty. He very well could have lost a huge chunk, if not all, of his income, depending on how his contract worked.

But that does not excuse using inappropriate (borderline derogatory) comments directed towards crypto users and the industry that he used at the recent Crypto Task Force Roundtable. We didn’t read the entire script. But the first page is more than enough.

Most of his tweets go back and forth between berating the current SEC and trash-talking crypto. This is another reason we think he may have had a paycheck that was dependent on the previous SEC regime.

Facts Don’t Lie

We don’t think these gentlemen are stupid. They’re clearly smart and capable individuals. But they’re wrong. And in a few cases, they could even be lying.

Why? Does it have to do with money? Are they looking for credibility for something? Are they reaching in an attempt to stay relevant in a pro-crypto atmosphere that’s quickly leaving their opinions in the dust and constantly proving them wrong and irrelevant?

Unfortunately, we can’t really answer those questions. All we can do is display facts, public receipts, and provide unbiased ideas on what could possibly be happening.

Facts don’t lie. People do. And the facts are that these gentlemen are wrong. Their arguments are moot, inaccurate, and even contradictory.

Wonder if the NYT will run our rebuttal…

Spoiler: They won’t.

But that’s fine. We’ll settle for being right.

About the Author